Medicare Part B premiums have consistently risen over the decades and are expected to keep climbing. These increases are largely driven by the growing cost of healthcare services, outpatient treatments, and prescription medications across the United States.

Most adults age 65 and older, as well as certain individuals under age 65 who qualify due to specific medical conditions, can enroll in Medicare coverage.

Enrollees may opt for Medicare Part A only, which covers inpatient hospital services. The majority of beneficiaries do not pay a monthly premium for Part A because of prior payroll tax contributions.

Alternatively, you can enroll in Part B, which helps cover outpatient care such as doctor visits, durable medical equipment, preventive services, and certain home health services. Part B requires payment of a monthly premium.

The amount you pay for Part B depends on your income level, and the standard premium generally increases from year to year. Reviewing the Medicare part b premium 2026 chart can help beneficiaries anticipate future costs and plan their retirement healthcare budget more effectively.

Medicare Part B premium increase data

The standard monthly Part B premium is $185 in 2025, and it has generally increased over time, starting at just $4 in 1970. This steady upward trend reflects inflation, expanded medical services, and higher overall healthcare spending.

The table below illustrates how Part B premiums have changed throughout the years, providing historical context for current and projected increases.

| Calendar year | Standard monthly premium |

|---|---|

| 1970 | $4 |

| 1975 | $6.70 |

| 1980 | $8.70 |

| 1985 | $15.50 |

| 1990 | $28.60 |

| 1995 | $46.10 |

| 2000 | $45.50 |

| 2005 | $78.20 |

| 2010 | $110.50 |

| 2015 | $104.90 |

| 2016 | $121.80 |

| 2017 | $134 |

| 2018 | $134 |

| 2019 | $135.50 |

| 2020 | $144.60 |

| 2021 | $148.50 |

| 2022 | $170.10 |

| 2023 | $164.90 |

| 2024 | $174.80 |

| 2025 | $185 |

Although the overall pattern shows growth, there have been minor decreases. For instance, premiums dipped slightly in 2000 compared to 1995, again in 2015 compared to 2010, and once more in 2023 compared to 2022.

Looking ahead, projections suggest continued increases. While these projected amounts are not yet finalized, they are often reviewed in resources such as the Medicare Part B premium 2026 overview to help beneficiaries stay informed about expected changes:

| Calendar year | Standard monthly premium |

|---|---|

| 2026 | 196.40 |

| 2027 | 210.60 |

| 2028 | 224.30 |

| 2029 | 240.10 |

| 2030 | 253.40 |

| 2031 | 268.80 |

| 2032 | 285.60 |

Monitoring the Medicare part b premium 2026 chart and future projections can be especially important for individuals on a fixed income, as even modest annual increases may affect long-term retirement planning and Social Security benefit allocations.

Medicare Part B and income-related monthly adjustment amounts (IRMAAs)

Beginning in 2007, beneficiaries with incomes above specific thresholds have been required to pay an income-related monthly adjustment amount (IRMAA) in addition to the standard premium.

Your IRMAA is determined using your reported income from 2 years earlier. For example, your 2025 IRMAA is calculated based on your 2023 federal tax return. This look-back period can be important if your income has recently changed due to retirement or other life events.

The 2025 IRMAA brackets and corresponding premiums are shown below:

| 2023 income: Individual | 2023 income: Married, filing jointly | 2023 income: Married, filing separately | 2025 monthly Part B premium |

|---|---|---|---|

| $106,000 or less | $212,000 or less | $106,000 or less | $185 |

| more than $106,000 up to $133,000 | more than $212,000 up to $266,000 | — | $259 |

| more than $133,000 up to $167,000 | more than $266,000 up to $334,000 | — | $370 |

| more than $167,000 up to $200,000 | more than $334,000 up to $400,000 | — | $480.90 |

| more than $200,000 up to$500,000 | more than $400,000 up to $750,000 | more than $106,000 up to $394,000 | $591.90 |

| $500,000 or more | $750,000 or more | $394,000 or more | $628.90 |

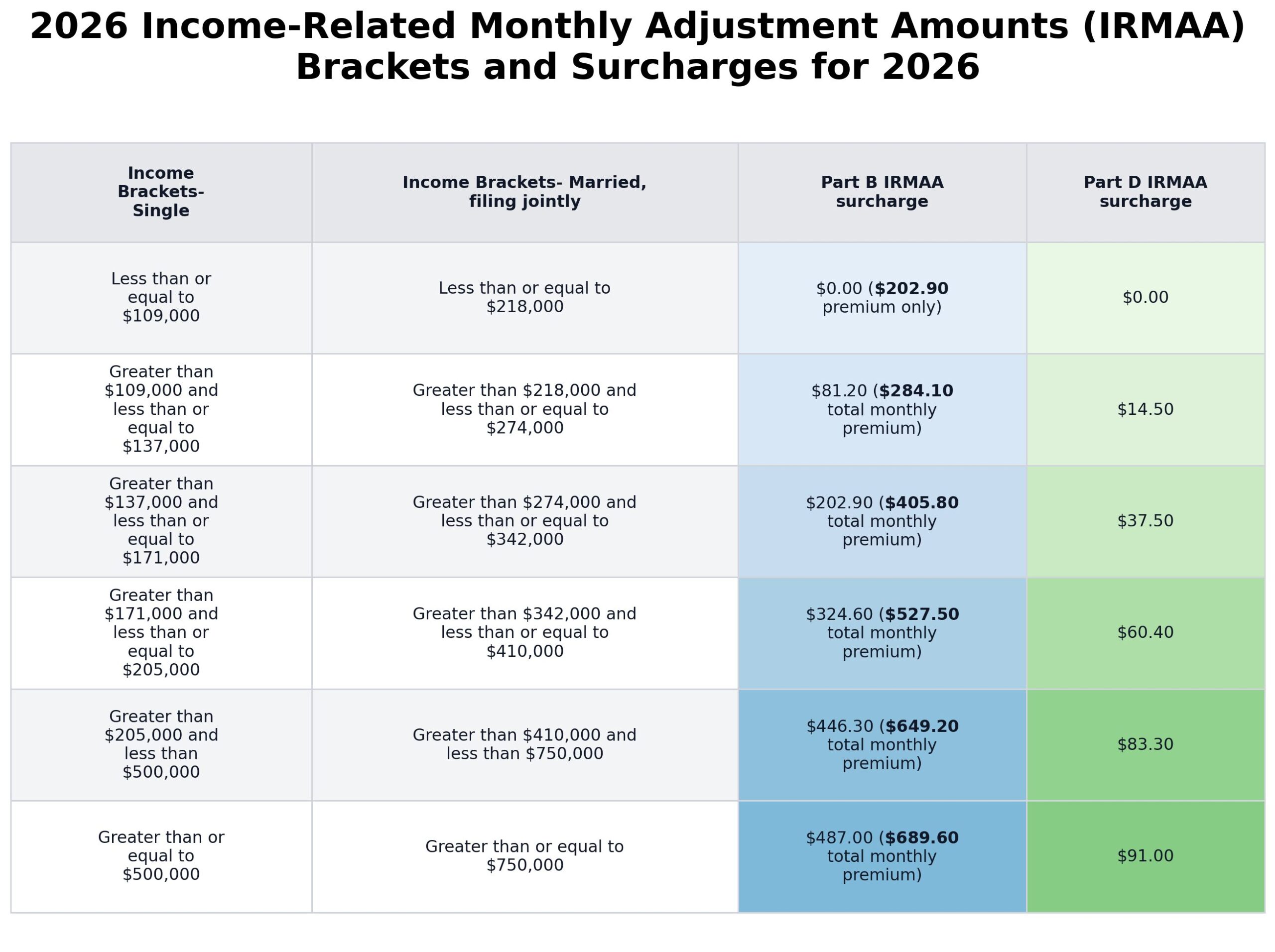

If inflation remains steady, the projected 2026 IRMAA brackets and related premiums, based on the 2024 Medicare Trustees Report, are expected to be:

| 2024 income: Individual | 2024 income: Married, filing jointly | Projected 2026 monthly Part B premium |

|---|---|---|

| $107,000 or less | $214,000 or less | $186.90 |

| more than $107,000 up to $134,000 | more than $214,000 up to $268,000 | $261.70 |

| more than $134,000 up to $169,000 | more than $268,000 up to $338,000 | $373.80 |

| more than $169,000 up to $202,000 | more than $338,000 up to $404,000 | $485.90 |

| more than $202,000 up to $500,000 | more than $404,000 up to $750,000 | $598.10 |

| $500,000 or more | $750,000 or more | $635.50 |

Projected figures for individuals who are married but file separately have not yet been released. Because IRMAA can substantially increase your monthly premium, reviewing both the Medicare part b premium 2026 chart and income brackets is essential for higher-income beneficiaries.

Other Part B costs

In addition to the monthly premium, beneficiaries must satisfy the annual deductible before Part B begins covering eligible services. In 2025 the deductible is $257. Updated information about the Medicare Part B deductible 2026 can help you estimate your total out-of-pocket healthcare expenses.

After meeting the deductible, you typically pay 20% coinsurance for many covered services, while Medicare pays the remaining 80%. This coinsurance applies to services such as physician visits, outpatient therapy, and certain medical equipment.

However, there are exceptions. In some cases, such as certain clinical lab tests and preventive care services, the deductible and coinsurance may not apply. Preventive services can include screenings, vaccines, and wellness visits designed to detect or prevent illness early, which may reduce long-term healthcare costs.

How is Part B financed?

Medicare is funded by two dedicated trust funds maintained by the U.S. Treasury:

- Hospital Insurance (HI) Trust Fund: This trust fund finances Medicare Part A.

- Supplementary Medical Insurance (SMI) Trust Fund: This trust fund supports Medicare Part B, Medicare Part D prescription drug plans, and Medicare’s administrative expenses.

The SMI Trust Fund is primarily funded through beneficiary premiums and general tax revenues. As healthcare utilization increases and medical technology advances, funding requirements may grow, contributing to gradual premium adjustments over time.

Takeaway

Since 1970, Medicare Part B premiums have shown an overall upward trajectory, with only a few modest declines along the way.

Current projections indicate that premiums are likely to continue rising in the coming years if inflation remains consistent. Reviewing the Medicare part b premium 2026 chart, understanding IRMAA thresholds, and accounting for the annual deductible and coinsurance can help you better prepare for future healthcare expenses under Medicare.

Leave a Reply

You must be logged in to post a comment.